Texas is #1 for tornadoes, wind & hail storms every year in the United States.

Austin Roofing Offers Free Storm Damage Inspections. If you have Storm Damage, We Will Stand In Your Corner & Speak With The Adjuster To Explain The Damage.

ROOFING CLAIMS PROCESS

1:

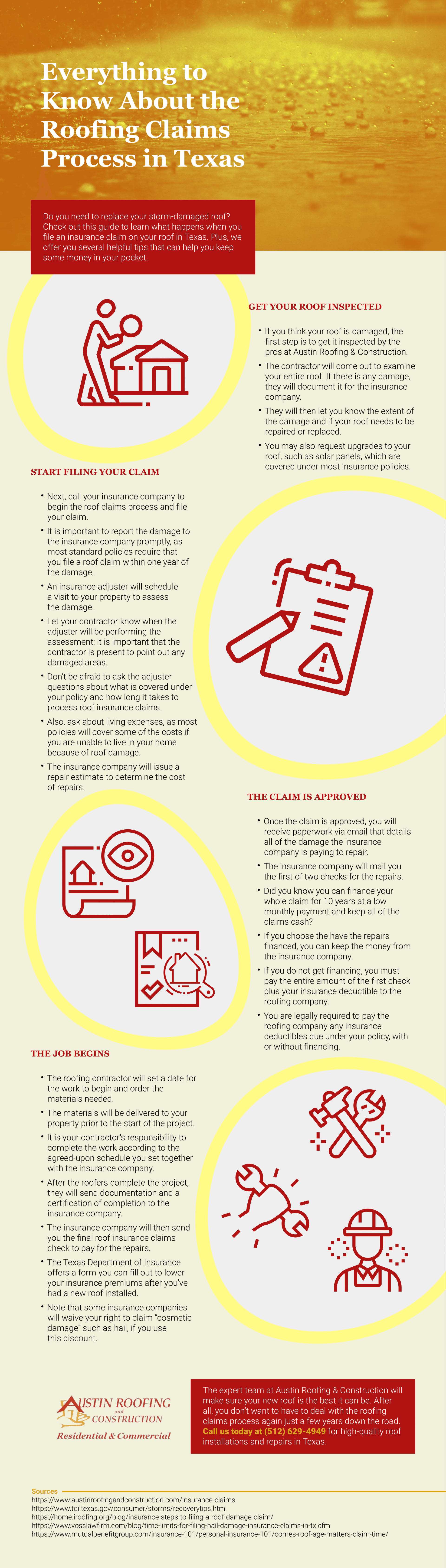

You suspect you have hail damage & probably want to file a claim if it is extensive.

2: Before proceeding with claims, it's crucial to address any urgent repairs to prevent further damage. Call a local roofing company immediately for an inspection. This ensures that any immediate threats to your roof's integrity are managed, minimizing additional costs or complications.

3: Call your insurance company to file the claim. Ensure you provide them with detailed information, including the roofer's assessment, to support your claim.

4:

The adjuster will call you to tell you when he/she will be out to inspect the damage. Being prepared with all necessary documentation and having your roofer's assessment on hand can facilitate a smoother inspection process.

5:

The claim is approved. You will receive the claims paperwork via email. This details all of the specific damage that the insurance company is paying to fix.

6: You will receive the first check called ACV (Actual Cash Value). This is the first of 2 checks. Sign & deposit into your bank account.

7:

Call the local roofing company that you have chosen. You will be asked to cut a check from your account for the amount of the 1st check plus your deductible.

Why?

8:

The project gets scheduled and all the work is done exactly as directed by claims paperwork.

9:

Upon completion of the project the roofing company will send documentation and certification of completion to the insurance company. Thus releasing the final check (Depreciation).

10: You deposit the last check into your account and then write your final check to the roofing company.

11:

You receive a thank you note from the roofing company. (Well you do if you choose us :)

12: Contact your insurance agent and let them know you have a brand new roof and to endorse your policy to reflect the new roof. This will often result in a reduced premium on your homeowners policy.

Texas Department of Insurance Offers a Form to Lower Home Insurance Premiums After Installation of a Class 4 Shingle / Metal Roof. Note That Some Insurance Companies Will Install the Discount but Will Also Waive Your Future Right to Claim "Cosmetic Damage" Such as Hail.

Texas Department of Insurance Impact Resistant Roofing Installation Form

FAQ

Q. What is the claims paperwork?

A.

This is the document detailing what areas the insurance company is paying to fix and how much they are paying for the work.

Q.Do I need to get all the work done that the claims paperwork specifies?

A. The insurance company will not re-insure items of the home not repaired. Meaning if the same area suffers damage later the insurance company will not authorize payment due to the item not being repaired in the last claim. Often there are follow-up inspections done to make sure the property was repaired to specifications.

NOTE - IF THERE IS A CERTAIN DETACHED STRUCTURE OR A PART OF YOUR HOME YOU NO LONGER WANT, NEED OR NEED TO HAVE INSURED, THEN YOU HAVE THE OPTION NOT TO REBUILD THAT PART OF YOUR PROPERTY. THE APPROVED CLAIM AMOUNT WILL BE REDUCED FOR WORK NOT COMPLETED.

Q.

What is ACV (Actual Cash Value)?

A.

It is the total replacement of the item cost minus depreciation.

Depreciation is the total price given to the amount that age & weathering have reduced the current market value of that item - in this case your roof.

To better understand roofing insurance, it's essential to compare Actual Cash Value (ACV) with Replacement Cost Value (RCV).

- Replacement Cost Value (RCV): This pays the full cost of replacing your damaged roof with a new one of a similar kind and quality. However, it deducts any applicable deductible, ensuring you receive a brand-new roof without worrying about depreciation.

- Actual Cash Value (ACV): As previously explained, ACV factors in depreciation based on your roof's age and condition. It reimburses you for the current market value of your roof, which may not cover the full cost of a new replacement.

When considering roofing insurance, understanding these differences can help you make an informed decision. RCV might be a preferable option if you want comprehensive coverage, while ACV might suit those looking for a more economical premium, acknowledging that full replacement costs may not be covered.

Q.

Do I call my agent or the company directly to file the claim?

A.

Have your agent help you file the claim. They are going to know the claims process and will make sure everything is

coded properly. Your future insurance rates will be affected by the "code" given to this damage claim.

Q.

Is the roofing company supposed to meet the adjuster?

A.

The adjuster typically likes to do his/her job without the assistance of a roofer. However, in the case that the claim is denied, it is a good idea to have the roofing company there to meet the adjuster for the re-inspection of the damage. A reputable roofer can provide valuable insights during these meetings, ensuring all necessary repairs are documented, which strengthens your claim.

Q.

Why do roofing companies ask for the claims paperwork?

A.

In most cases, the roofing company is who will be submitting completion documents to the insurance company to certify all work has been done to specification. Without the claims paperwork, we cannot submit final paperwork to the insurance company. Additionally, having access to this paperwork allows the contractor to provide expert guidance throughout the claims process, helping you avoid any missteps that could delay or reduce your settlement.

Furthermore, a skilled contractor can work with insurance adjusters to negotiate a fair settlement. This collaboration often increases the likelihood of a satisfactory outcome. Alongside these services, hiring a professional roofing company ensures quality workmanship. They use the best materials and installation techniques, guaranteeing that your roof remains durable and long-lasting.

Q.

Why is payment from the insurance company made with 2 separate checks?

A.

The insurance companies like to have leverage to make sure the work gets completed. This is due to claims being paid in the past where the property was never repaired / replaced.

Q.

Do I have to pay my deductible? There are companies who say I don't have to pay it.

A. In order to get full payment from the insurance company someone has to submit paperwork indicating that the deductible has been paid.

Texas HB 2102 effective September 1st, 2019

: The new law creates a Class B misdemeanor offense of 180 days in county jail and a fine of up to $2000, for (1) a business who sells goods or services to provide such a good or service in such a prohibited manner (violating contractor), (2) an insured (policyholder)who commits an offense if the person, in connection with a first party claim knowingly submits or allows a claim to be submitted in violation of subsection c, (the violation section directly above) unless the insured person promptly notifies the insurer of the violation.

Q. What if I don't have the funds to pay my deductible?

A.

We offer financing for all credit types with options to pay over time. Typical loan periods are 2 - 12 years.

Q. I spent the first check already but I really need to get the work done!

A. We offer financing for all credit types with options to pay over time. Typical loan periods are 2 - 12 years

Q. Can I get an upgraded roof? Examples: Metal / Hail Resistant Shingle

A. Yes you can! You just pay/finance the difference in price.

Q. Do I get a new roof discount from my insurance company now?

A. Some insurance companies will issue a new roof discount once completion has been certified. Click Here to download this TDI form to give to your insurance company if you have a Class 4 roofing material.

Q. Is my new roof a class 4 hail resistant material?

A. Some are and we can give you a form certifying this for your insurance company. You may get up to a 20% discount on your homeowner's insurance! NOTE: You will give up future claims for "cosmetic damage" like hail unless it actually makes holes through your roof.

Form

Q. Is there a warranty on my new roof?

A. We offer workmanship warranties, (free leak repairs due), up to 25-years for shingles & 10-years for metal. We also include a 50-year material warranty for manufactures' defect.

Q. Will my insurance premiums go up after a storm damage claim?

A. It is against the law for an insurance company to increase your home owners insurance premium based on payment / claim of storm damage.

Why a Professional Roof Inspection is Crucial Before Filing a Claim

Navigating the aftermath of a storm can be daunting, particularly when assessing the impact on your roof. The damage isn't always noticeable from the ground, which is why enlisting the expertise of a professional roof inspector is essential.

Here's why:

Unseen Damage Detection

Professional inspectors have the keen eye needed to spot damage that might go unnoticed by the untrained eye. This includes:

- Creased or Cracked Shingles: These issues often hide beneath undisturbed exterior layers, escaping casual observation.

- Hail and Wind Damage: Inspectors can identify hail impact and wind effects that might not be visible without close scrutiny.

Informed Decision-Making

Having a comprehensive evaluation enables you to make a well-informed decision about filing a claim. Many property owners, even those initially doubtful, find that their claim success increases with professional validation of the damage.

Claim Approval Success

A credible assessment from a qualified inspector can significantly boost the likelihood of your insurance claim being approved. Insurance adjusters value detailed reports and evidence from trained professionals, increasing your chance of a favorable outcome.

Additional Benefits of Hiring a Professional Roofer

- Peace of Mind: Trustworthy roofers handle the claims process, alleviating stress and saving you valuable time.

- Efficient Repairs: Reputable contractors are known for completing projects on time, minimizing disruptions to your daily routine.

- Warranty Coverage: Many professional roofing companies offer warranties, ensuring your roof's long-term protection and providing ongoing confidence in their work.

By investing in a professional roof inspection, you're not only protecting your property but also ensuring you have the necessary information to navigate insurance claims effectively. Furthermore, hiring a professional roofer brings additional benefits that extend beyond the immediate task, offering peace of mind and reliable service in the long run.

Here's a breakdown to guide your decision:

Assess the Age and Condition of Your Roof

- Lifespan: Determine how old your roof is. Most roofing materials have a finite lifespan. For instance, asphalt shingles typically last about 20-25 years.

- Current Damage: Assess the extent of the damage. Minor leaks or missing shingles might be manageable with simple repairs.

Cost Analysis: Repair vs. Replace

- Short-term vs. Long-term Costs: Repairs generally incur lower immediate costs, but frequent fixes can add up. Replacement might be a larger upfront investment but can save money over time.

- Material Costs: Consider the price differences between repair materials and new roofing materials. Energy-efficient or more durable options might offer savings in the long run.

Insurance and Warranty Considerations

- Insurance Coverage: Check what your homeowner's insurance will cover. Some policies may not fully cover the cost of replacement if the roof is old.

- Warranties: Evaluate existing warranties on your current roof and the potential warranties on new roofing options. A new roof may offer better warranty protections.

Potential Benefits of Replacement

- Energy Efficiency: New roofing technologies can enhance energy efficiency, potentially lowering utility bills.

- Increase in Property Value: A new roof can increase your home's market value, offering a possible return on investment.

Pros and Cons of Each Option

- Repairs: Suitable for minor damage but might be a recurring expenditure if the roof is nearing the end of its life.

- Replacement: Offers durability and potential cost-efficiency over time, though with a larger initial expense.

By balancing these considerations and understanding the long-term impacts, you can make an informed decision on whether to repair or replace your roof. Always consult with a reputable roofing professional to assess your specific situation and get tailored advice.

Why Insurance Companies Might Fully Cover an Older Roof Replacement

When dealing with an older roof, insurance companies may surprisingly be more willing to cover the cost of a full replacement.

Let's break down why this might be the case:

- Challenges in Repair: Older roofs, due to their wear and tear over time, can be significantly more difficult to repair than newer ones. The materials might have decayed or been discontinued, making repairs both challenging and often more costly.

- Storm Damage Impact: Ageing roofs are typically more vulnerable to damage from storms, wind, or hail. If such damage occurs, insurance companies might deem a full replacement more cost-effective than repeated patch repairs over time.

- Comprehensive Coverage Criteria: While age alone doesn't qualify for coverage, the extent of damage combined with the roof's condition can influence an insurance company's decision. They aim to restore the home to its pre-damage state, which might necessitate a complete roof overhaul if repairs aren't viable.

In essence, although age isn't directly covered, the increased susceptibility and repair difficulties associated with older roofs can lead insurance companies to authorize a full replacement, ensuring the homeowner’s protection and satisfaction.

How Does the Age of My Roof Impact My Decision to File an Insurance Claim?

When deciding whether to file an insurance claim for your roof, its age plays a crucial role in determining the best course of action.

The Age Factor

- Older Roofs:

- Durability Concerns: Roofs nearing the end of their lifespan, typically around 25 years old, may seem like a poor candidate for insurance coverage. Surprisingly, insurance companies might cover a complete replacement in such cases.

- Repair Challenges: Older shingles become brittle and difficult to manipulate. If individual shingles are damaged by wind or hail, attempting to replace them can cause surrounding shingles to crack. Insurance providers often prefer replacing the entire roof rather than risk further damage through inadequate repairs.

- Newer Roofs:

- Repair Feasibility: With less wear and tear, newer roofs can often be repaired without harming other shingles. Insurance companies might only cover repairs, which could mean the cost doesn't justify filing a claim if it doesn’t meet your deductible.

- Claim Implications: Filing a minor claim for a newer roof might not be economically beneficial. You risk adding unnecessary claims to your insurance record, which may affect future policy terms.

Key Considerations

- Extent of Damage: Assess whether the damage is significant enough to justify a claim. For newer roofs, substantial damage might necessitate a claim, but the threshold is higher compared to an older roof.

- Financial Impact: Calculate the potential cost versus benefit of a claim. It's crucial to weigh the deductible against the repair or replacement cost covered by insurance.

- Future Implications: Consider the long-term effects on your insurance record. Multiple claims can impact your premiums or eligibility for coverage in the future.

In summary, the age of your roof influences whether an insurance claim is sensible. Evaluate the damage, consider your deductible, and think about future insurance implications before making a decision.

How Hail Damage Impacts Roof Shingles' Structural Integrity

Hail damage might not result in immediate leaks, but it can significantly weaken the strength and durability of roof shingles.

Here's how it happens:

- Granule Loss: When hailstones strike, they often dislodge the protective granules on shingles. These granules are crucial as they shield the shingle from UV rays and other weather elements. Once they are gone, the shingle becomes more susceptible to further damage.

- Fiberglass Mat Damage: Beneath the surface layer of granules lies the fiberglass mat, which provides structural support. Hail impact can fracture this mat, compromising the shingle's overall integrity. This damage often isn't visible at first glance but can lead to significant issues over time.

- Progressive Deterioration: After the initial impact, the compromised shingles will continue to degrade. The combination of granule loss and cracks means the shingles can’t effectively protect your roof structure. Eventually, these weakened shingles might fail, leading to potential leaks and other costly repairs.

For these reasons, insurance companies often opt to replace the entire roof after severe hail storms to prevent future failures and expensive claims.

Understanding the Challenge of Detecting Creased Shingles

Creased shingles can be deceptively hard to identify, yet they play a crucial role when assessing damage for an insurance claim. Unlike missing shingles, creased ones remain in place, making them less obvious to the untrained eye. However, the impact of high winds can bend these shingles, causing them to develop hidden breaks or creases on the underside.

Why Creased Shingles Matter

- Hidden Vulnerability: While creased shingles may appear intact, their structure is compromised. The bending motion from the wind can cause tiny fractures, allowing rainwater to seep underneath and damage the layers of the roof.

- Interference with Water Shedding: A primary function of shingles is to efficiently direct rainwater away from the roof. When creased, they lose this ability, leading to water absorption along the crease and further degradation over time.

- Potential for Widespread Damage: Without visible signs of damage like missing shingles, homeowners might mistakenly believe their roof is undamaged. However, the subtler damage from creasing can be just as severe, potentially leading to extensive interior damage if ignored.

Implications for Insurance Claims

- Hidden Damage Recognition: Insurance claims often rely on visible damage indicators. Yet, creased shingles highlight the importance of recognizing less obvious signs that still compromise the roof's integrity.

- Consideration of Roof Age and Ventilation: The decision to replace a roof may still be influenced by additional factors like age and ventilation. Even when only creased shingles are present, these factors might sway an insurance company to support a full roof replacement.

In essence, while creased shingles might not catch your eye at first glance, their impact is significant and warrants keen inspection, especially when filing an insurance claim.

How Can Discontinued Shingles Affect an Insurance Claim for Roof Damage?

When dealing with roof damage, the availability of shingle materials can significantly influence the outcome of an insurance claim. Let’s explore how discontinued shingles can impact this process.

- Understanding Insurance Policies

- Most insurance policies stipulate the use of "like kind" materials for repairs. This means when a single shingle or a section is damaged, insurers look to replace it with identical or similar products.

- The Complication of Discontinued Shingles

- If the shingles on your roof are discontinued, this complicates things. Replacement of these specific materials can become difficult or impossible. As a result, insurance companies might be obligated to replace not just a few shingles but the entire roof.

- The Claim Approval Process

- Should the insurer be unable to match the damaged shingle with a "like kind" product, replacing the whole roof may be the only feasible solution. In such cases, claims tend to receive approval, as full roof replacement ensures uniformity and longevity.

- Homeowner Awareness

- Unfortunately, many homeowners are unaware if their shingles have been discontinued. Regularly checking the status of your roofing materials can be advantageous, potentially strengthening your case should you need to file a claim.

- In summary, discontinued shingles can lead to comprehensive roof replacements under insurance policies, provided the insurer cannot source an equivalent material for smaller repairs. This unique situation often works in favor of the homeowner when filing claims.

Challenges of Repairing Older Roof Shingles

Repairing older roof shingles poses unique difficulties due to their age and condition. When a single shingle requires replacement, the surrounding shingles must be lifted to fit the new piece in place. Unfortunately, older shingles tend to become brittle and inflexible over time. This lack of pliability makes them prone to cracking or breaking during the repair process.

Consequences of Using Newer Materials:

- Potential for Increased Damage: Every attempt to replace just one shingle may inadvertently harm adjacent shingles, leading them to crack. This could set off a ripple effect of damage across the roof.

- Insurance Limitations: Insurers may decline to cover repairs that risk causing further structural damage. They often avoid fixing issues that could result in more extensive repairs in the future.

Hence, these challenges typically necessitate considering a complete roof replacement. It minimizes the risks and ensures the home remains protected over the long term, without introducing further complications from piecemeal repairs.

The Role of Ridge Vents in Insurance Decisions for Roof Damage

When considering whether to file an insurance claim for roof damage, understanding the structure and components of your roof can significantly influence your decision, especially the presence of ridge vents.

How Ridge Vents Influence Coverage

- Determining Damage Claims: If your roof includes ridge vents, each slope may be treated separately. This means the insurance company might only cover the damaged slope, leaving the rest untouched.

- Continuous Roofing Systems: Without ridge vents, your roof is often seen as one continuous structure. In such cases, damage to one slope might result in coverage extending to all slopes, offering potentially broader repair or replacement options.

Factors to Consider Before Filing a Claim

- Extent of Damage: Limited damage, such as missing a few shingles on one slope, might not warrant a claim, particularly if you've got ridge vents.

- Age and Wear of the Roof: A newer roof, say around five years old, with minor damage, might not be worth the insurance hassle, especially if you're dealing with a deductible.

- Scope of Coverage Necessity: Extensive damage or discontinued shingles can make filing a claim more appealing if your roof lacks ridge vents.

Ultimately, the decision to file a claim can hinge on how your roof is ventilated. Ridge vents can lead to a more segmented approach in insurance assessments, impacting whether you decide to move forward with a claim or handle repairs out of pocket.

Understanding the Role of Roof Ventilation in Insurance Coverage Decisions

When assessing whether to pursue an insurance claim for roof damage, the type and condition of your roof's ventilation system can significantly influence the decision.

Importance of Roof Ventilation

Proper roof ventilation, like ridge vents, plays a vital role in the overall health and durability of a roof. It helps prevent moisture buildup and reduces the risk of problems such as mold or premature aging of materials. This can influence whether damage is extensive and impacts insurance considerations.

Factors in Insurance Decisions

- Type of Ventilation:

- Ridge Vents: If your roof is equipped with ridge vents, it might experience better airflow, potentially limiting damage to specific areas. In cases with minimal issues, such as a few missing shingles, filing an insurance claim might not be necessary. The cost of repairs could be less than your deductible.

- Lack of Ventilation: Roofs without adequate ventilation might suffer from more extensive damage, making claims more justifiable.

- Extent and Age of Damage:

- Minor damage on a well-ventilated roof, particularly if it's relatively new (e.g., around 5 years old), might not necessitate a claim. Conversely, older roofs or those with widespread issues, even with proper ventilation, often merit filing due to potential internal consequences.

- Discontinued Materials and Loss Severity:

- If shingles are discontinued, this can complicate repairs, possibly increasing costs and making insurance claims worthwhile despite any existing ventilation system.

In summary, while a well-ventilated roof might minimize damage, the extent and specifics of the situation—age, material availability, and damage breadth—are crucial when deciding to file an insurance claim. Evaluate these factors carefully to make an informed decision.

What should homeowners understand about their insurance coverage before proceeding with roof repairs?

Understanding Your Insurance Coverage for Roof Repairs

When you're considering roof repairs, it's crucial to grasp the details of your insurance coverage. Here are the key points every homeowner should be aware of:

Review Your Policy

1. Coverage Verification: First, examine your homeowner's insurance policy to confirm whether weather-related damage is included. It's essential to know your deductible and understand the maximum amount your policy will cover.

2. Trend Awareness: Stay informed about changing insurance practices. For instance, insurers are increasingly hesitant to cover roofs that are 20 years old or older, especially if they're made from materials like asphalt, which deteriorate faster compared to metal or tile roofs.

Types of Coverage

Understanding the difference between the two main types of coverage—Replacement Cost Value (RCV) and Actual Cash Value (ACV)—is critical:

- Replacement Cost Value (RCV): This coverage pays for the entire cost of replacing your damaged roof. You'll receive a new roof of similar kind and quality, minus your deductible.

- Actual Cash Value (ACV): With ACV, the payout reflects depreciation based on the roof’s age and condition. This means you'll get the current market value of your roof, which might not fully cover replacement costs.

Before starting any roof repair, thoroughly reviewing and comprehending these aspects of your insurance policy can save you from unexpected financial burdens.

How should homeowners review and compare settlement offers from insurance adjusters?

How Homeowners Can Evaluate Settlement Offers from Insurance Adjusters

When you're faced with a settlement offer from an insurance adjuster, it's crucial to carefully assess and compare the proposal to ensure you're receiving a fair deal. Here's how to go about it:

1. Obtain Contractor Estimates: Start by gathering detailed repair or replacement estimates from reputable contractors. Their assessments will provide a comprehensive view of the potential costs involved with the necessary repairs.

2. Compare Details: Examine both the adjuster's offer and your contractor's evaluation side by side. Look for discrepancies in the scope of work, materials, and costs outlined in each.

3. Identify Discrepancies: Pay attention to any differences in coverage scope. Are there specific repairs or upgrades your contractor included that the adjuster omitted?

4. Open Communication: If your contractor's evaluation highlights areas of concern, discuss these with the adjuster. Engaging in open dialogue can sometimes resolve misunderstandings or errors in the initial assessment.

5. Negotiate for Fairness: If there's a significant gap between the two estimates, enlist your contractor's assistance in negotiating a better settlement. Contractors often have experience dealing with insurance claims and can provide valuable insights during discussions.

6. Final Decision: Remember, the objective is to reach a settlement that adequately covers the repair costs required to restore your property to its pre-loss condition. Trust your contractor's expertise, but also be willing to compromise to achieve a satisfactory resolution.

By systematically reviewing and comparing the details, you're more likely to secure a settlement offer that aligns with your needs.

How can homeowners verify if their insurance policy covers weather-related roof damage?

Verifying Weather-Related Roof Damage Coverage in Your Homeowner's Insurance

Ensuring your roof is protected against weather-related damage requires a thorough understanding of your homeowner's insurance policy. Here’s a step-by-step guide to help clarify your coverage:

1. Check Your Policy Documentation

- Review Coverage Terms: Dive into your policy details to find specific terms related to weather-related damage. Pay particular attention to the coverage description and what incidents are defined as covered events.

- Note Deductible and Limits: Understand both the deductible amount—the out-of-pocket cost before insurance kicks in—and the overall coverage limits.

2. Understand Coverage Types

- Replacement Cost Value (RCV): This option provides funds to replace your damaged roof with a new one of similar kind and quality, minus your deductible.

- Actual Cash Value (ACV): This factors in depreciation, paying only the current market value, which could be less than the full replacement cost.

3. Stay Informed on Insurance Trends

- Age and Material Restrictions: Some policies may have restrictions for older roofs, often those 20 years or older. Roofs made from materials such as asphalt tend to receive less favorable terms due to their relatively shorter lifespan compared to metal or tile options.

4. Consult with Your Insurance Provider

- Directly contact your insurer to clarify any doubts. They can provide insights into how specific factors, such as your roof's age and materials, influence your coverage.

By taking these proactive steps, homeowners can ensure their roofs are adequately covered against unpredictable weather damage.

What are the time limits for filing an insurance claim?

What Are the Time Limits for Filing a Roofing Insurance Claim?

When it comes to filing a roofing insurance claim, understanding the time limits is crucial. While the specific deadlines can differ from one insurance provider to another, there are general guidelines you can follow.

- Standard Filing Period: Most insurance companies set a standard period of approximately one year from the date of damage to file a claim. However, this timeframe is not universal, so checking with your specific insurer is essential.

- Post-Storm Extensions: In the event of significant weather events, some insurers may offer extended filing periods. These extensions acknowledge the widespread damage and the increased number of claims following a major storm.

- Check Your Policy: Always review your insurance policy for any particular deadlines or conditions. Policies might include distinct clauses based on the type of damage or the nature of the claim.

Essentially, the key is to act promptly and communicate with your insurance provider to ensure you're within the allowed window. This proactive approach can prevent complications and enhance your chances of a successful claim.

What precautions should be taken when hiring a roofing contractor after a storm?

Precautions for Hiring a Roofing Contractor After a Storm

After a storm, finding a reliable roofing contractor is crucial. Taking the right precautions can save you from future headaches and ensure quality repairs. Here’s what you need to do:

Don’t Rush the Process

It's tempting to quickly choose a contractor to repair storm damage, but haste can backfire. If you rush, you might end up with limited options. Instead, invest time in exploring multiple contractors. This way, you can compare different estimates, reputations, and skill levels to make a sound decision.

Research and Value Quality

Storms often keep reputable roofing companies busy, so patience can be a virtue. If your situation isn’t urgent—for instance, there's no active leak—consider waiting a bit to hire a trusted professional. Check their credentials, read reviews, and review examples of their past projects to ensure they deliver high-quality service.

Gather and Compare Estimates

Your insurance adjuster or roofing specialist might point out storm damage, but it’s your duty to secure the right contractor. Don’t settle on the first estimate you receive. Request quotes from multiple contractors to evaluate fair pricing and quality assurance. This approach also enables a comprehensive assessment of each contractor’s terms.

Know Your Insurance Details

Before work begins, clearly understand what your insurance policy covers. The contractor will coordinate with your insurance adjuster to make sure the repair quote is inclusive. It’s crucial for you to thoroughly review your coverage, including any deductibles and costs for optional upgrades, so there are no surprises along the way.

By following these strategies, you can confidently navigate the post-storm repair process and hire a roofing contractor who meets your needs and standards.

What steps should homeowners take to avoid roofing scams after severe weather?

How Can Homeowners Prevent Roofing Scams After Severe Weather?

Surviving severe weather is tough enough without falling victim to roofing scams. Here’s how you can protect yourself and make wise decisions when hiring a contractor.

Evaluate Before You Commit

Tempting as it may be to quickly fix your roof, take a moment to breathe and weigh your options. Scrutinize potential contractors instead of hastily signing a contract. Hasty decisions often bind you to unfavorable terms if the contractor’s abilities or pricing don’t match your expectations.

Prioritize Due Diligence

Busy contractors are typically those deemed reputable, especially after a storm. Your roof may endure slight delays if there’s no immediate damage, providing you the chance to hire a proven expert. Delve into the contractor's history: check credentials, read reviews, and assess their portfolio to ensure they deliver satisfactory workmanship.

Solicit Multiple Quotes

Finding hail damage doesn’t end your responsibility. After your insurance evaluation, it’s essential to gather multiple bids from diverse contractors. This practice not only gives you a look at fair pricing but also lets you gauge the quality you should expect. Seek at least three quotes to better compare different offers and terms.

Leverage Subheadings for Precise Action Steps

Here’s a recap:

- Take Your Time: Avoid immediate commitments.

- Research Thoroughly: Focus on quality and trust.

- Request Multiple Estimates: Always compare.

By following these steps, homeowners can navigate post-storm repairs with confidence, significantly reducing the risk of falling prey to scams.

What happens if the insurance company does not cover all submitted items?

Understanding Out-of-Pocket Costs

When Insurance Falls Short

When your insurance company doesn't cover all the items you’ve submitted, it's crucial to know your financial responsibilities before any work commences. Here’s what you should expect:

1. Initial Quote: The contractor should supply you with a detailed out-of-pocket estimate. This ensures you're aware of any costs that insurance won't cover, allowing you to budget accordingly.

2. Pre-Installation Inspection: To minimize unexpected expenses, thorough inspections should be conducted prior to starting the project. This includes checking for potential issues such as damaged flashing or rotten decking in the attic, which might not be apparent initially.

3. Transparent Communication: Should additional costs arise during the installation—perhaps from unforeseen issues or necessary adjustments—the contractor must inform you immediately. Clear communication prevents surprise expenses and allows peace of mind as the work progresses.

4. Final Agreement: Once you're equipped with all the necessary information, ensure a clear and documented agreement is in place, outlining both covered and uncovered costs. This will safeguard against misunderstandings and offer clarity for both parties involved.

Taking these proactive steps will help manage your roofing project smoothly, even when insurance coverage has its limitations.

What examples of storm damage might be covered by insurance?

Storm Damage That Insurance Might Cover

When a storm hits, the damage can be extensive and worrying. If you're wondering what types of storm damage might be covered by your insurance, here's a rundown:

1. Roof Damage

Storms often wreak havoc on roofs, causing issues like:

- Broken or torn roof shingles

- Missing shingles, exposing your home to the elements

2. Hail Damage

Hail can be particularly destructive and might affect:

- Shingles, resulting in dents or granule loss

- Gutter systems, leading to reduced water drainage

- Soft metal components, such as vents

- Glass structures, including skylights

3. Water Damage

Heavy rain can lead to:

- Leaks in the roof or ceiling

- Water seepage into the home's interior

4. Wind Damage

Strong winds may cause:

- Fallen branches hitting the roof or other parts of the house

- Debris striking and damaging exterior walls or windows

5. Structural Damage

In more severe cases, storms can lead to:

- Compromised structural integrity of walls or foundations

- Damage to outdoor structures, such as sheds or fences

Remember to review your policy details or consult your insurance provider to confirm the coverage specifics for each type of damage.

What if my insurance company approves more than the cost of my estimate?

When your insurance company approves an amount greater than your repair estimate, several outcomes may occur based on their policies:

1. Utilizing Excess Funds:

Some insurers might allow you to use the surplus to manage any additional related expenses. This could include unexpected repairs that arise or enhancing certain aspects of the project.

2. Refunding the Difference:

Alternatively, the insurance provider might require you to return the excess amount. This process will follow specific procedures set by your insurer.

3. Company-Specific Policies:

Every insurance company has unique guidelines for handling these situations. It's crucial to refer to your policy details or directly consult with your insurance representative to understand their approach.

To ensure a smooth process, always communicate openly with your insurer and confirm their procedures before making any decisions on handling extra funds.

How do previous roof claims affect the likelihood of approval for a new claim?

Submitting a successful roof insurance claim often hinges on the initial approach. Insurance companies generally have policies that favor addressing legitimate claims promptly. However, repeated submissions for the same issue can complicate matters significantly.

Impact of Multiple Claims

1. Decreased Approval Chances: If you've previously filed roof claims, insurers may scrutinize subsequent claims more intensely. Each additional attempt might reduce the likelihood of approval.

2. Preexisting Damage Concerns: When examining a second or third application for similar roof damage, adjusters might argue that the damage is preexisting. This happens especially if it's linked to a previously rejected claim.

3. Adjusters’ Constraints: Insurance adjusters have a duty to verify claims thoroughly. They often view multiple claims for the same damage as suspect, further diminishing the odds of decision in your favor.

To maximize approval chances, aim to ensure the first claim is comprehensive and well-documented. By presenting all necessary evidence initially, you can strengthen your position and avoid the pitfalls of multiple submissions.